Last year, Expedia, Inc.’s CEO, Dara Khosrowshahi, received a mind-boggling 881 percent raise, making his total compensation $94.6 million, more than the combined earnings of actors Bradley Cooper and Tom Cruise. In the eyes of corporate boards, CEOs are superstars, providing revenue and shareholder growth as well as an “extraordinary ability” to predict risk that the market cannot.

The public, however, isn’t happy with CEO paychecks, even though it actually tends to underestimate how much CEOs are paid. According to a 2016 survey by researchers at Stanford University, the typical American believes that Fortune 500 CEOs make approximately $1 million a year. In reality, however, the average Fortune 500 CEO makes a staggering $12.2 million a year. Of the 1,202 survey respondents, 74 percent said that they disapprove of the ratio of CEO to average worker compensation, and 62 percent believe that CEOs should not earn beyond a certain amount, regardless of the company’s size or performance. In a hypothetical situation in which a company’s value increases by $100 million in a year, the median respondent believes that the CEO should receive just half a percent, or $500,000, as compensation.

This couldn’t be further from the kind of compensation packages currently in practice. The Hartford Courant reports that Mark Bertolini, chairman and CEO of Aetna, received $27.9 million in compensation in 2015, up from $15 million the previous year. Meanwhile, Aetna’s other top executives earned a combined $35.47 million. David M. Cordani, CEO of Cigna Corp., received $49 million in 2015, up by 80 percent from the previous year.

If we are to recover from the Great Recession, the Economic Policy Institute estimates that wages for private employees must rise by 3.5 to 4 percent a year. For CEOs, however, the EPI finds that, between 1978 and 2014, inflation-adjusted compensation rose astronomically—997 percent, dwarfing the 10.9 percent increase for workers. In 1965, the CEO-to-worker compensation ratio was 20 to 1; by 2014, it was 303 to 1. Bloomberg reports that CEO-to-employee pay in the U.S. is more than twice what it is in Switzerland and Germany, and about 10 times greater than in Austria.

Does this imply that U.S. CEOs are more than 300 times smarter than the average employee? An EPI report concluded that CEO compensation growth does not, in fact, reflect the market for talent, but rather the presence of economic rents. In other words, the pay doesn’t reflect the productivity of the CEO, nor the demand for skills in a particular sector, but rather “the power of CEOs to extract concessions.” The report’s authors suggest that, if CEOs earned less or were taxed more, there would be no adverse impact on either output or employment.

Dean Baker, co-director of the Center for Economic Policy Research, agrees. “There’s a lot of evidence that the market for CEO pay doesn’t work because you don’t have the market discipline that you would have typically,” he says. “So, an ordinary worker, their employer says, ‘Well, we’re paying you $30,000 or $40,000 a year because you contribute that much to our output. They may not always get that right, but at least they have a clear basis for assessing it, and there’s a clear person responsible for making that decision. For the CEO, in principle, it’s the corporate directors who are supposed to say, ‘We pay you $15 million a year; do you contribute that to the company? Can we get someone who can contribute just as much, and can we pay them $5 million or $3 million?’ In principle, they’re supposed to ask that question. It doesn’t seem they ask that, though.”

That’s because directors have little interest in stirring the pot: They receive very attractive paychecks for a part-time job—$100,000 a year for attending six to 12 meetings. Moreover, CEOs invariably play a big role in getting directors their positions. “So, there’s very, very little incentive to say, ‘Look, you’re getting paid too much. There are plenty of people out there who do the same thing for half the price,’” Baker says. “Instead, the directors tend to go along and say, ‘Well, the CEO of the other company got a $1 million raise? Sure, we’ll give you $1 million—we’ll give you $2 million.’”

If the CEO wasn’t getting paid all this money, where would the funds go? Primarily to shareholders, Baker says. “It comes out of what companies will reinvest and out of other workers’ pay.”

In other words, contrary to popular belief, board composition does not impact executive pay. As a consequence, corporate wage distribution tends to favor top-tier employees. In a paper titled “Executive Salaries and Their Justification,” George P. Brockway writes:

When the CEO of a corporation accepts, as one did in 1982, a year’s compensation of $51 million (salary, bonus, stock option), he can scarcely be comfortable in the executive dining room unless his principal assistants are paid well up in the millions, while their assistants must be paid in the hundreds of thousands, and so on down the line. Meeting such a payroll must, at the very least, inhibit the corporation from lowering its prices.

Inflated wages at the top are of particular concern in the health care industry. The Centers for Medicare & Medicaid Services estimate that health care spending in the U.S. surged to $3 trillion—or $9,523 per person—in 2014, accounting for 17.5 percent of GDP.

“A huge portion of this is coming directly from taxpayers,” Baker says. “If you count the implicit tax subsidy for employer-provided health insurance, way over half of health care is paid for by the public sector. Private insurers are getting a very large share of their money from taxpayers.”

Wendell Potter, former public relations executive for Cigna Corp., told MedCity News in June 2015: “There’s no doubt that one of the reasons why Americans pay more for health insurance and for health care than people in any other country in the world is because of this high executive compensation.”

Not everyone agrees.

“The typical CEO of the largest 500 companies earns about $10 million per year,” says Brian Tayan, one of the authors of the Stanford University study. “This is less than a tenth of a percent of the company’s market cap and less than a percent of the profits. In health care, we don’t see CEOs making substantially higher pay. I would be skeptical of claims that their pay is material to health care costs.”

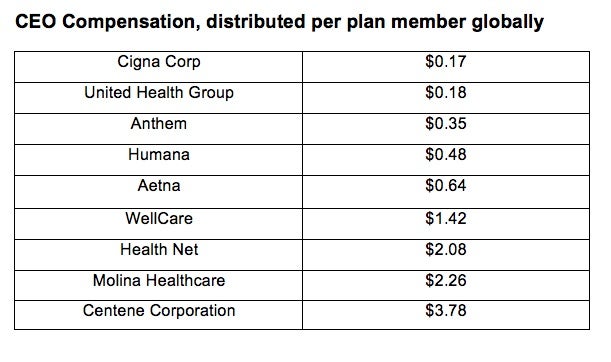

However, in a March 2016 rebuttal column in Forbes, Chris Conover discusses what would happen if we redistributed the CEO compensation for large health insurers to members. The answer, he says, is peanuts, at least when you look at the annual cost of CEO compensation per plan member globally.

But politicians aren’t buying it, especially when government incentives are involved. Connecticut State representative Susan Johnson (D) has proposed mandating municipal property tax payments for nonprofit hospitals that award executives more than $500,000 in annual compensation. And many health care executives make a lot more than that. The Stamford Advocate reports that Stamford Hospital president and CEO Brian Grissler earned $2.4 million from 2013 to 2014; Western Connecticut Health Network CEO and president John Murphy also received $1.2 million for the period.

“I looked at the salaries of hospital administrators. That’s the amount of money we were trying to save for the hospitals,” Johnson says. “They’re worth a good salary, but they’re not worth millions of dollars. These hospitals are supposed to provide services to the community—that’s why we give them nonprofit status at the federal level. What they should be doing is paying for the CEO salaries at those high rates themselves. One way to address that was to say, ‘If you have that kind of money to pay your chief executive officer such a high salary, then you should also be able to pay the local property tax.’”

In fact, as early as 2010, David Albert Bjork announced that legislators plan to extend the $500,000 limit on executive pay at banks (imposed by the Troubled Asset Relief Program) to tax-exempt health care organizations. Hospital boards, however, believe that higher pay attracts better talent and results in better patient care. But that’s not necessarily the case: A 2014 study published in the Journal of the American Medical Association found that compensation of CEOs at nonprofit hospitals is not associated with patient outcomes or community benefits.

Still, many economists believe that legislators should refrain from manipulating the price system. “To intervene with prices is always going to cause distortions. If the salaries of the CEOs of nonprofit hospitals are rising, it’s an indication that the number of people who can do that work is relatively low compared to the number of hospitals that need them to do that work,” says Howard Baetjer, a libertarian economist at Towson University. “If salaries above a certain threshold triggered a penalty for the hospital, then it’s likely that some hospitals would try to avoid that by hiring someone who won’t do as good a job. That ultimately would mean inferior service for the patients.”

Tayan also believes that capping pay would lead to worse outcomes. “You are more likely going to chase away the best people, who will work in other sectors where they can be rewarded,” he says. The solution? To improve disclosure. That way, shareholders have a better understanding of the packages that directors are offering and of how pay correlates with performance. “Much of the outrage we see is due to the public not understanding why the pay is deserved,” Tayan says. “Most Americans have no problem with pay and success if they believe the pay is merited.”

At the heart of all this data is a compelling narrative: Sooner or later, for every employee, it comes down to “what’s in it for me?”

“Becoming aware of the top leadership awarding itself pay hikes, perks, and bonuses while the rest of the company is undergoing budget cuts has a very negative effect on people,” HR executive Agata Dulnik of Accenture says. “Employees begin to question the integrity of their leadership, develop a negative attitude to change initiatives, and lose loyalty. Their engagement drops, and they start to actively look for a way out.”

But that’s not all, she says. In an age of social media and blogs, word of such practices gets out quickly and takes on a life of its own, affecting the company’s image not just with employees, but also with potential employees and consumers. Last year, for instance, JPMorgan Chase & Co. chairman and CEO Jamie Dimon received a $7 million pay raise, earning $27 million at a time when 6,761 employees were laid off. And that’s just one of many examples. To his credit, however, Dimon decided to raise the minimum pay for 18,000 employees, mostly bank tellers and customer service representatives, from $10.15 an hour to between $12 and $16.50 an hour. “A pay increase is the right thing to do,” he said in a LinkedIn post. “Wages for many Americans have gone nowhere for too long.”

Still, not everyone’s impressed. Dimon’s post drew scathing comments like these:

“Allmost to [sic] generous, it means allmost $21k a year. The staff can buy new socks for x-mas.”

“What difference does it make if you earn $10 or $11? I guess you could buy more chewing gum.”

Another reader wrote: “Let them eat cake!”