If you have a life insurance policy, that means your insurance company pays your beneficiaries when you die, right? Turns out, the answer is: um, sometimes. A new Florida law requires life insurance companies to actually contact the beneficiary of a policy and pay them when the policy-holder dies—something they apparently often don’t do unless a claim is filed. That behavior might be unethical, but it’s perfectly logical for a profit-oriented company.

The very concept of life insurance can be morally troubling. In a 1978 paper, Viviana A. Zelizer described how people in the early nineteenth century shied away from the product, which seemed to tie together death and commerce. But, she writes, by the end of the century, many people accepted a counterbalancing argument that not buying insurance was its own moral failing.

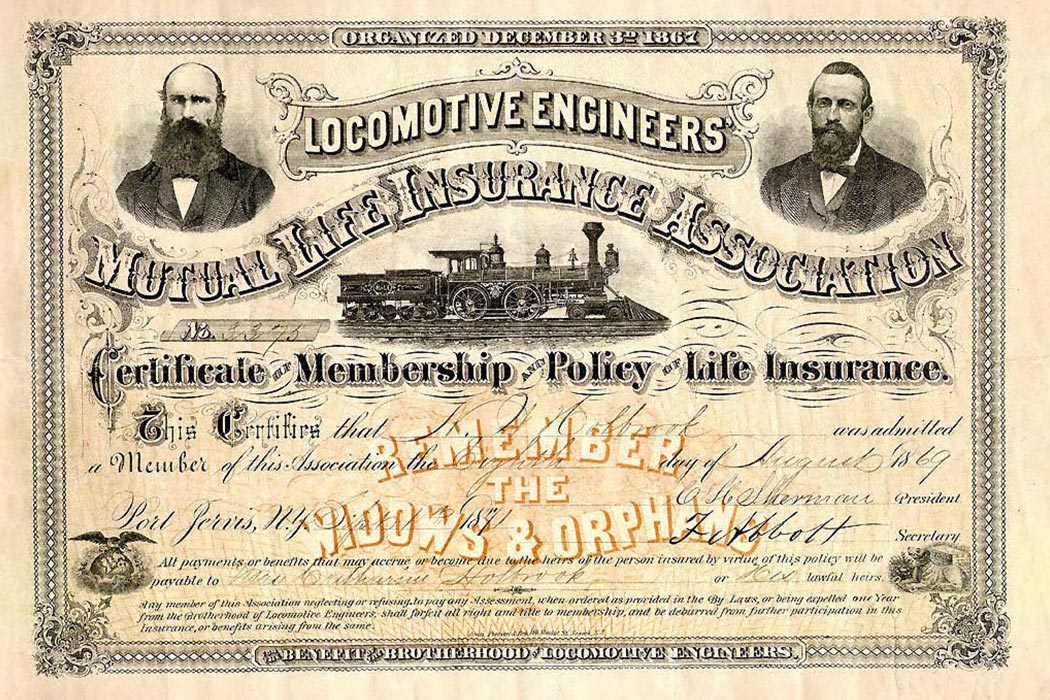

In the eighteenth century, before the advent of life insurance, widows and orphans typically inherited enough land that they could support themselves. They could also expect help from neighbors and from mutual aid groups. Similarly, neighbors and relatives handled the physical work necessary to bury the dead. Then early in the nineteenth century, with fire and marine insurance becoming increasingly popular, new companies were formed to sell life insurance. State legislatures quickly granted them charters, but the public was mostly uninterested in the new product.

Zelizer writes that it’s no surprise that people didn’t like the concept at first. Since ancient Rome, Western law had held that a man’s life could not be given a monetary value. Many critics of the day made a similar argument. The Mennonite Church, which threatened to excommunicate any member who insured his life, warned that the practice “is equivalent to merchandising in human life.”

To some, the idea of life insurance evoked superstitious fears. A booklet published by one insurance company quoted a common objection made by wives: “It would make me miserable to think that I were to receive money by your death. … It seems to me that if [you] were to take a policy [you] would be brought home dead the next day.”

It was only toward the middle of the century that life insurance began to catch on. The country was urbanizing—the percentage of Americans living in urban areas doubled between 1840 and 1960. As families left productive rural households for city life, they typically became completely dependent on a male earner’s wage. At the same time, they left behind the support systems of extended families and neighbors. Insurance companies argued that a man would be judged harshly by friends and relatives after his death if he didn’t make sure his family would be provided for.

Religious leaders began to embrace the need for insurance. “Once the question was: can a Christian man rightfully seek Life Assurance?” Rev. Henry Ward Beecher asked in 1870. “That day has passed. Now the question is: can a Christian man justify himself from neglecting such a duty?”

Considering how morally conflicted we’ve always been about life insurance, perhaps it’s not that surprising to see the ethics of the enterprise back in the news.