On August 26, 1920, the United States officially adopted the 19th Amendment to its Constitution, granting women nationwide the right to vote for the first time. Though incomplete—in practice, it mostly enfranchised white women nationwide and many Black women in the North and the West—it was the single largest expansion of voting rights in the nation’s history. But even this recognition of the rights of basic citizenship failed to ensure equality. One of the biggest hurdles women of that era faced wasn’t civic at all. It was economic.

To be truly equal in an ever more capitalist United States, you needed control over your money. You needed access to a bank.

Weekly Newsletter

"*" indicates required fields

For most of modern history, both in the US and the rest of the world, women had only a small fraction of the financial independence enjoyed by men. Even the richest women were, legally speaking, often not wealthy themselves. They were instead the wives and daughters of rich husbands and fathers, and that meant strict dependence on the men in their lives and an ever-present danger that all they had could be taken away.

There were, of course, rare outliers—women with access to financial services, even before such access was guaranteed by law. Noblewomen like the Countess of Castlemaine appear in the earliest surviving bank record in Britain dating to the seventeenth century. But these are exceptions; for the most part, lacking in legal protections, most women were locked out of the financial system.

In the eighteenth century, there were small but significant advances in women’s economic rights. In 1771, a few years before the American Revolution began, the colony of New York passed the “Act to Confirm Certain Conveyances and Directing the Manner of Proving Deeds to Be Recorded.” This awkwardly-titled law was part of a subtle revolution; it was among early laws requiring men to get the signed permission of their wives to sell property she brought into the marriage. Almost 70 years later, Mississippi became the first state to allow women to own property outright in their own names. Any perceived patina of progressiveness here is illusory; the property Mississippi allowed women to own was restricted to slaves.

In 1848, the same year as the first women’s rights convention in Seneca Falls, New York state took the lead again by granting married women the right to collect rent, own their own property, and enter contracts. Importantly, it also removed their liability from their husband’s debts in certain situations. It took another 52 years for every state to adopt similar laws. The deeply sexist arguments against these laws often overlapped significantly with those against women’s suffrage: women were unable to perform the regular duties of men in the economy, and that allowing them to do so would upend civilization itself, plunging the nation into chaos.

The passage of the Homestead Act in 1862 signaled one of the most important advancements in the economic rights of women. Infamous for encouraging the seizure of land in the American West from native tribes in the service of pioneer settlement and for exposing indigenous people to colonial violence, the legislation offered many women their first opportunity to own property. Under the terms of this law, any woman—single, widowed, divorced, or abandoned—could claim up to 160 acres of land for herself and in her own name. In some territories, up to 20 percent of land claims were made by women. Yet for women who were unwilling or unable to move West, there remained few options for building wealth.

This inequality presented an opportunity first recognized and exploited by a criminal. Sarah Howe, a fortune teller by trade who had been previously arrested for fraud, opened the first notable women’s bank in Boston in 1879, having observed that the city’s upper and middle-class ladies needed a place to grow their savings.

The Ladies’ Deposit Company was a new kind of bank, entirely and exclusively devoted to women. About 1200 of them deposited a total of $500,000, equivalent to almost $15 million adjusted for inflation. They were each promised a return of 8 percent a month, and for a while, they got it. Yet reporters at the Boston Daily Advertiser soon discovered that Howe was paying returns with the deposits of new clients. Howe operated what in today’s argot is a Ponzi scheme, though Charles Ponzi was not born until 1882, proving that women can’t catch a break even when it comes to having fraud named in their honor.

Howe’s company, and several others she established to replicate the scam in the following years, became well-known in the newspapers of the 1880s and may have soured people for a time on the establishment of banking institutions catering exclusively to women. Indeed, it took another 40 years for a second women’s bank—a reputable one, this time—to be founded in the United States.

Meanwhile, the struggle for women’s suffrage raged on. Though the right to vote was their primary goal, economic rights were certainly on the minds of leading 19th century suffragists. “Woman must have a purse of her own, & how can this be, so long as the wife is denied the right to her individual and joint earnings,” wrote Susan B. Anthony in her diary in 1853. “Reflections like these, caused me to see and really feel that there was no true freedom for woman without the possession of all her property rights.”

Long-awaited change was clearly in the air in the fall of 1919. Congress had already passed the 19th amendment, and it was working its way through state legislatures on its way to ratification. On October 6, 1919, the First Woman’s Bank opened in Clarksville, Tennessee. True to its name, it was founded by Brenda Vineyard Runyon, a prominent community leader and head of the local Red Cross, and served women primarily, but not exclusively. The Clarksville Leaf-Chronicle described the bank as “petticoated from president to janitress,” and by the end of its first day of business, it had more than $20,000 in new deposits, a figure that soon exceeded $100,000 (over $1.7 million today) for years. Never a financial giant, the bank was nevertheless “an important factor in the business circles of this and the surrounding counties,” according to the Leaf-Chronicle.

When First Woman’s began to struggle in 1926, it was absorbed by the First Trust and Savings Bank of Clarksville. Bigger fish kept swallowing smaller ones, as banks tend to do, but it never completely closed, and survived under one name or another through the Depression and subsequent calamities until it came under the massive umbrella of Bank of America.

Decades later, the Tennessee Historical Quarterly reminded its readers proudly that “with the current attention to equal rights for women and the development of a number of women’s banks, one must consider that the first bank in the United States managed totally by women was formed in a small conservative southern city fifty-seven years ago and operated successfully for nearly seven years.” As it happens, it was also Tennessee that officially delivered women’s suffrage to the United States, when it became the 36th state to ratify the 19th amendment on August 18, 1920.

When the Great Depression came in 1929, it devastated banking. Nine thousand banks closed for good during the 1930s, including over 4,000 in 1933 alone. The Depression was a disaster of some degree to nearly every household in the country, but it led to a surprising rise in employment among women. The industries most devastated were those dominated by men—banking, but also mining, manufacturing, and construction. Men’s unemployment led their spouses to look for work outside the home for the first time in their lives, though their pay was much lower than their husband’s.

This shift was largely a phenomenon among white women, and their gainful employment came at a cost to women of color. “White women replaced black women by moving down the occupational ladder of desirability,” according to historian Lois Rita Helmbold. “For black women already on the bottom rung, there was no lower step, and they were effectively pushed out of the labor force.”

The jobs that were most available to women—sewing, laundering clothes, cleaning houses, and clerical work—barely paid enough to keep families afloat. Even slightly higher-paying positions, primarily schoolteachers and nurses, paid poorly. These newly employed women were unable to build wealth, without which, they had no need for a bank of their own.

World War II brought about another, even more massive, spike in the number of working women. They moved into industrial jobs that had long been the domain of men, now gone to war. Between 1941 and 1944, the number of American working women rose by 67%, from 10.8 million to 18 million. Wages rose too. In the Boston area, women who had been making $18 a week in 1941 could make up to $70 a week in a Remington ammunition plant by war’s end.

After the war, millions of middle-aged and older women remained on the shop floor and banks were poised to cater to their needs—both as customers and as employers.

By 1955, about a third of all bank employees in the United States were women. At first, these jobs were overwhelmingly in the companies’ lower ranks. Women were employed as “calculators,” behind the scenes operating the machines doing the math. Through the 1950s and 60s, women started showing up more often in the front of the bank, as what the sociologist Rosemary Crompton described as “a new and largely feminine occupation—the cashier-clerk.”

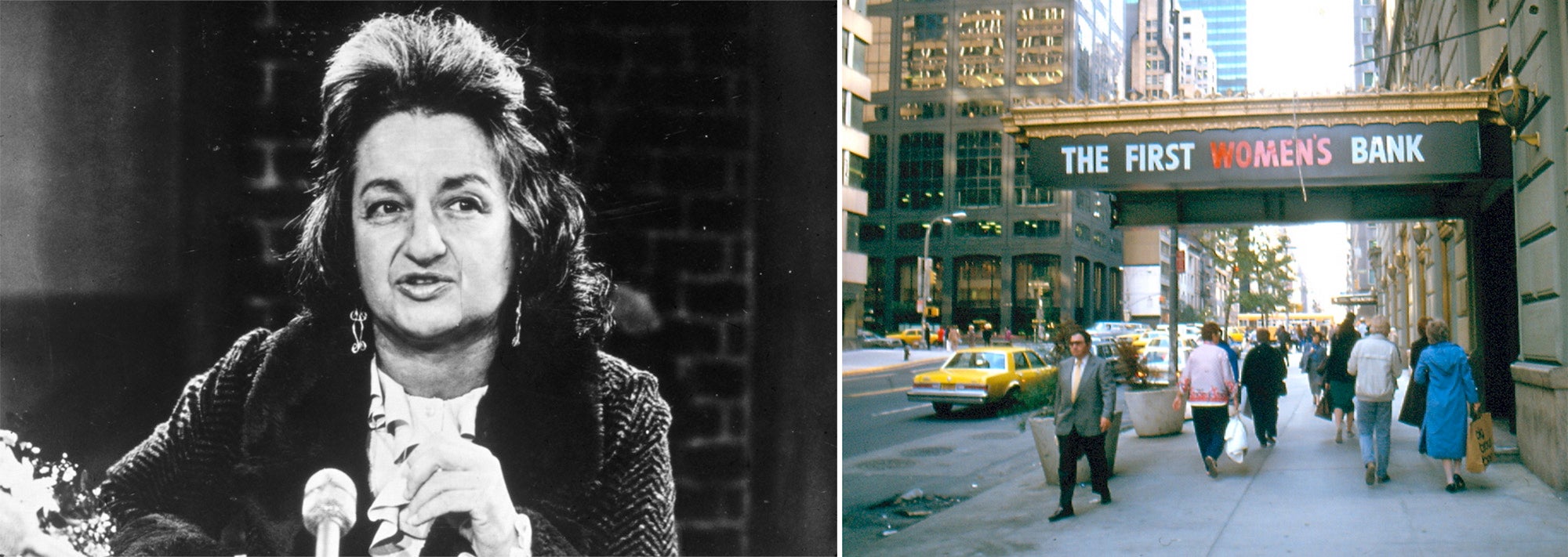

In the meantime, governments began to recognize the need to enshrine financial rights. The Equal Credit Opportunity Act of 1974 gave every American woman, married or not, the right to open her own bank or credit account. It outlawed discrimination by both sex and race in banking. It is easy to forget today that this right has existed nationally for fewer than fifty years. The next year, The First Women’s Bank of New York opened, with feminist icon Betty Friedan famously among its first depositors. In a striking parallel to the original First Woman’s Bank in Tennessee, it struggled after its well-publicized opening. The bank removed the word “women” from its name in 1989, and closed in 1992.

Both patterns though—regulatory expansion and the opening of new women’s banks—repeated all over the world. In Ireland, women gained the right to own their home outright, without a man, in 1976, a right American women had gained nationwide in 1900. By 1978, even Abu Dhabi, a conservative emirate where a man held official power over all of his wife’s property and affairs, had a thriving and popular women’s bank. Men were banned from entering the building, including the bank manager himself.

Today, banking access for women is nearly universal, at least on paper. Yet significant inequalities still exist in practice. Beyond the stubborn wage gap that remains between men and women doing the same job, bank and credit gaps endure as well, resulting in an even larger wealth gap. In 2021, American households headed by women owned only 55 cents for every dollar of wealth owned by male-headed ones. Women’s income and wealth are also more vulnerable than men’s in crisis conditions. A sobering example of this persistent inequality came in 2020, when the economic downturn at the start of the COVID-19 pandemic caused four times more women to leave the labor force than men.

The women’s bank is largely a thing of the past, but survives in the form of two very different descendants. As banking has gone digital, several startups have launched aimed specifically at banking services for women. In the less developed world, microfinance, where both institutions and individuals give small loans to support local business, overwhelmingly goes to rural women. Women are also increasingly taking the reins as CEOs and leaders of major banks, though still not at a rate representative of their population. After centuries of slow and imperfect progress, there are still obstacles to overcome, and inequalities to challenge.

{kind=link}